Índice8 secciones

The valuation of distressed companies represents one of the most complex challenges in corporate finance, requiring advisors to navigate between fundamentally different value paradigms. As restructuring activity surged 34% in 2024-2025 amid rising interest rates and tightening credit conditions, the ability to accurately assess whether a struggling enterprise holds greater value as a going concern or through liquidation has become increasingly critical for creditors, equity holders, and restructuring professionals.

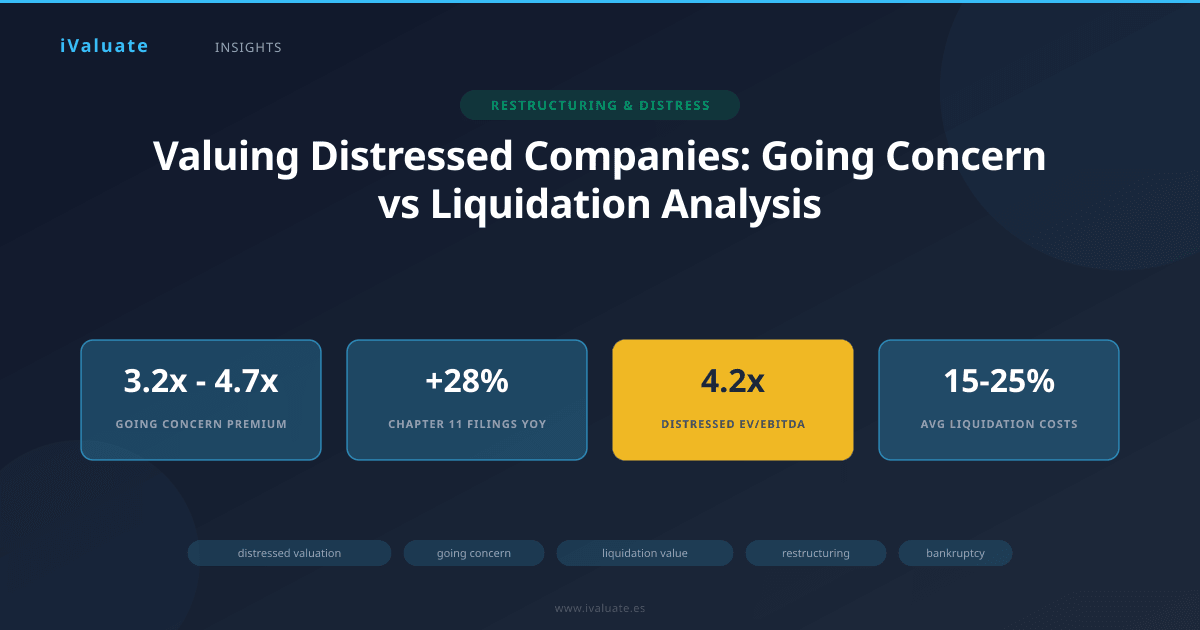

The distinction between these valuation approaches is not merely academic—it drives fundamental decisions about whether to pursue operational turnarounds, recapitalizations, or asset sales. In the current environment, where Chapter 11 filings among mid-market companies increased 28% year-over-year through Q1 2025, understanding when to apply each methodology can mean the difference between maximizing recoveries and destroying residual value.

01 The Fundamental Dichotomy: Going Concern vs Liquidation Value

At its core, going concern value assumes the business will continue operating indefinitely, generating cash flows that can be discounted to present value. This approach values the enterprise as an integrated operating entity, capturing the synergies between assets, the value of assembled workforce, customer relationships, and operational momentum. Going concern valuations typically employ discounted cash flow (DCF) analysis, comparable company multiples, or precedent transaction analysis—the same methodologies used for healthy companies, albeit with significant adjustments for distress factors.

Liquidation value, conversely, represents the net proceeds that would be realized if the company ceased operations and sold its assets piecemeal. This approach recognizes that an integrated business may be worth less than the sum of its parts when those parts can be redeployed more productively elsewhere. Liquidation scenarios range from orderly liquidation value (OLV), where assets are sold over a reasonable marketing period, to forced liquidation value (FLV), where time constraints necessitate fire-sale pricing.

The gap between these values can be substantial. In a 2024 analysis of 147 restructuring situations, going concern values averaged 3.2x the orderly liquidation value for manufacturing companies and 4.7x for technology and service businesses where intangible assets predominate. However, this premium narrows dramatically—or even inverts—when operational distress is severe or industry conditions deteriorate.

The Break-Up Value Consideration

Between pure going concern and full liquidation lies break-up value—the sum-of-the-parts valuation where different business units or asset groups are valued separately, some as going concerns and others on a liquidation basis. This hybrid approach has gained prominence in recent restructurings, particularly for conglomerates or companies with distinct operating segments that might attract different buyer pools.

A representative 2024 case involved a diversified industrial manufacturer with three divisions: a profitable aerospace components business, a marginally profitable automotive parts division, and a loss-making legacy industrial equipment segment. The break-up analysis valued the aerospace division as a going concern using 8.5x EBITDA (based on strategic buyer multiples), the automotive division using orderly liquidation of equipment and working capital, and the industrial segment on a forced liquidation basis. The resulting break-up value of $340 million exceeded both the standalone going concern value ($285 million) and full liquidation value ($180 million), ultimately driving the restructuring strategy toward a controlled asset sale process.

02 When Going Concern Value Applies: The Viability Assessment

The appropriateness of going concern valuation hinges on a rigorous assessment of operational and financial viability. Despite current distress, a company merits going concern treatment when several conditions align:

Sustainable Competitive Position

The business must possess defensible competitive advantages that support long-term cash generation. This includes proprietary technology, strong brand equity, exclusive supplier or customer relationships, regulatory licenses, or market position that cannot be easily replicated. A distressed specialty pharmaceutical company with valuable drug approvals and development pipeline, for instance, typically warrants going concern analysis even with current cash flow challenges, as these assets lose substantial value outside the operational context.

Solvable Capital Structure Issues

Financial distress must be distinguishable from operational distress. Companies facing temporary liquidity constraints or overleveraged balance sheets—but with sound underlying operations—are prime candidates for going concern valuations supporting recapitalization or debt restructuring. The key test: would the business generate adequate returns on capital if the balance sheet were right-sized?

Current market conditions have created numerous examples. A regional healthcare services provider entering Chapter 11 in late 2024 demonstrated EBITDA margins of 18% and consistent market share gains, but carried unsustainable debt from a 2021 leveraged buyout at peak valuations. The going concern valuation of $520 million (7.2x forward EBITDA) supported a debt-for-equity swap that reduced leverage from 8.5x to 3.2x, enabling emergence as a viable enterprise. Liquidation analysis had suggested only $280 million in recoveries, as the company's value resided primarily in operational systems, workforce expertise, and payer relationships that would dissipate in a wind-down.

Realistic Path to Profitability

For companies currently unprofitable, going concern valuation requires credible evidence that operational improvements or market conditions can restore positive cash flows within a reasonable timeframe—typically 12-24 months. This demands detailed operational turnaround plans with specific, achievable milestones, not aspirational projections.

The analysis must stress-test assumptions rigorously. In the current environment, where input costs remain elevated and consumer spending shows increasing selectivity, overly optimistic turnaround projections have led to failed restructurings. A 2024 study of unsuccessful Chapter 11 cases found that 67% had relied on going concern valuations with revenue growth assumptions exceeding realistic market potential, ultimately requiring conversion to liquidation when performance targets proved unattainable.

Adequate Liquidity for Restructuring

Going concern value is only relevant if the company can maintain operations through the restructuring period. This requires either sufficient cash reserves, committed debtor-in-possession (DIP) financing, or creditor forbearance. Without adequate liquidity runway, theoretical going concern value becomes moot as the business deteriorates toward forced liquidation.

DIP financing availability has tightened considerably in 2024-2025, with average commitment sizes declining 22% and pricing increasing 180 basis points compared to 2022-2023 levels. This liquidity constraint has forced more companies toward rapid asset sales rather than operational restructurings, even when going concern value theoretically exceeds liquidation value.

03 When Liquidation Value Dominates: Recognizing Terminal Decline

Liquidation becomes the appropriate valuation framework when fundamental business viability cannot be established or when asset redeployment creates superior value. Several indicators point toward liquidation-based valuation:

Structural Industry Decline

When the entire industry faces permanent contraction due to technological obsolescence, regulatory changes, or fundamental demand shifts, going concern assumptions become untenable. The value resides in redeploying assets to more productive uses, not continuing current operations.

The retail sector has provided numerous examples. Traditional department stores and specialty retailers facing e-commerce disruption have increasingly been valued on liquidation bases, as store leases, inventory, and fixtures command higher values in alternative uses than supporting declining retail operations. A 2024 analysis of retail bankruptcies showed that orderly liquidation values averaged 87% of book value for inventory and 45% for fixtures and equipment, while going concern valuations (when attempted) consistently proved overstated as sales continued deteriorating through restructuring processes.

Irreparable Operational Damage

Some distressed situations involve operational deterioration so severe that the business cannot be stabilized. Key customer losses, workforce exodus, supplier terminations, or reputational damage may have destroyed the operational foundation necessary for going concern value. In these cases, liquidation maximizes recoveries by monetizing assets before further value erosion.

A technology services company that entered bankruptcy in early 2025 illustrates this dynamic. Following a data breach and subsequent loss of three major clients representing 58% of revenue, the company faced cascading operational failures: key technical staff departed, remaining clients accelerated contract terminations, and vendor credit lines were withdrawn. While the initial restructuring plan assumed going concern value of $95 million based on historical multiples, rapid operational deterioration forced conversion to orderly liquidation within 90 days, ultimately realizing $52 million primarily from intellectual property sales and equipment disposition.

Superior Alternative Use Value

Sometimes assets command premium values in alternative deployments that exceed their value supporting current operations. Real estate holdings in appreciating markets, equipment with strong secondary markets, or intellectual property with broader licensing potential may drive liquidation value above going concern value.

This scenario has become increasingly common in the industrial sector. A manufacturing company occupying waterfront property in a gentrifying urban area may find that real estate values (for residential or mixed-use development) exceed the present value of manufacturing cash flows. Similarly, specialized equipment may command higher prices from growing competitors or adjacent industries than its value supporting a declining operation.

Insufficient Stakeholder Support

Restructuring requires cooperation from multiple stakeholders—creditors, equity holders, employees, customers, and suppliers. When this consensus cannot be achieved, liquidation may be the only executable path, regardless of theoretical going concern value. Contentious stakeholder dynamics, particularly among creditor classes with conflicting interests, can make operational restructuring impractical.

The rise of aggressive distressed debt investors has complicated this landscape. In several 2024-2025 cases, creditor groups holding blocking positions have pushed for liquidation strategies that maximize their specific recoveries, even when going concern alternatives might generate greater total value. This dynamic particularly affects middle-market companies where creditor groups are concentrated and individual positions are large enough to drive strategy.

04 The Valuation Methodologies: Technical Considerations

Going Concern Valuation in Distressed Contexts

Applying traditional valuation methodologies to distressed companies requires substantial adjustments. The discounted cash flow approach remains foundational, but several parameters demand careful recalibration:

Discount Rate Adjustments: The weighted average cost of capital (WACC) must reflect elevated risk. Distressed companies typically face equity costs of capital ranging from 25-40%, compared to 10-15% for healthy peers. Debt costs reflect actual borrowing rates (often 12-18% for DIP or exit financing in current markets) rather than pre-distress levels. The resulting WACC often exceeds 20%, substantially reducing present values compared to healthy company benchmarks.

Cash Flow Projections: Management projections require rigorous scrutiny and typically warrant significant haircuts. Best practice involves developing multiple scenarios (base, downside, and upside cases) with probability weightings, rather than relying on single-point estimates. Revenue assumptions must be stress-tested against customer concentration, competitive dynamics, and market conditions. Cost structures should reflect realistic operational improvements, not aspirational targets.

Terminal Value Considerations: The perpetuity growth assumption that drives terminal value in healthy company DCF models requires particular care in distressed contexts. Using normalized industry growth rates (typically 2-3%) may be inappropriate if the company's competitive position has been permanently impaired. Many practitioners apply reduced terminal growth rates (0-1%) or use exit multiples based on distressed precedent transactions rather than healthy company comparables.

Comparable Company Multiples: When using market multiples, selecting appropriate comparables becomes challenging. Using healthy peer multiples without adjustment overstates value, while using only distressed comparables may understate value if the subject company has better recovery prospects. A common approach applies a distress discount of 30-50% to healthy peer multiples, calibrated to the specific situation. In current markets, EV/EBITDA multiples for distressed companies average 4.2x compared to 9.8x for healthy peers in the same industries—a 57% discount.

Liquidation Valuation Approaches

Liquidation analysis requires detailed, asset-by-asset assessment using recovery rates derived from actual market transactions and appraisal data:

Orderly Liquidation Value (OLV): Assumes assets are sold over a reasonable marketing period (typically 6-12 months) with adequate time to identify buyers and negotiate terms. Recovery rates vary significantly by asset class: inventory typically realizes 60-85% of book value depending on obsolescence and seasonality; machinery and equipment achieves 40-70% based on age, condition, and secondary market depth; real estate often approaches fair market value with proper marketing; and accounts receivable recover 70-90% after bad debt reserves.

Forced Liquidation Value (FLV): Reflects compressed timeframes (30-90 days) necessitating discounted pricing. Recovery rates typically run 30-50% below OLV, with inventory realizing 35-60% of book value and equipment achieving 25-45%. Forced liquidation scenarios arise when liquidity constraints, lease terminations, or creditor actions prevent orderly wind-down.

Liquidation Cost Considerations: Both OLV and FLV must account for substantial wind-down costs: professional fees (legal, accounting, auctioneers) typically consume 8-15% of gross proceeds; employee severance and retention costs; lease termination penalties; environmental remediation; and warranty/return obligations. Net liquidation proceeds often run 15-25% below gross asset recovery values after these costs.

A detailed 2024 liquidation analysis for a mid-market distributor illustrates these dynamics. Gross asset values totaled $87 million (inventory $52M, receivables $23M, equipment $8M, real estate $4M). Orderly liquidation recovery rates of 75% on inventory, 85% on receivables, 55% on equipment, and 95% on real estate yielded gross proceeds of $72 million. After liquidation costs of $11 million, net OLV reached $61 million—70% of book value. Forced liquidation analysis suggested only $43 million net proceeds, a 30% reduction from OLV.

05 The Decision Framework: Integrating Multiple Perspectives

Sophisticated restructuring analysis rarely relies on a single valuation approach. Instead, best practice involves triangulating across methodologies and considering multiple stakeholder perspectives:

The Creditor Lens

Secured creditors focus intensely on liquidation values as their downside protection. Asset-based lenders typically advance 80-85% of eligible receivables and 50-65% of eligible inventory, implicitly assuming orderly liquidation scenarios. When going concern value falls below liquidation value plus a reasonable margin, secured creditors often push for asset sales rather than operational restructuring.

Unsecured creditors and subordinated debt holders, conversely, benefit from going concern premiums and typically support operational restructurings when viable. This creates natural tension in restructuring negotiations, with outcomes often determined by the relative leverage of different creditor classes.

The Equity Perspective

Equity holders retain value only when going concern value exceeds total debt obligations—a rare outcome in true distress situations. However, equity often retains nuisance value through bankruptcy process delays or litigation threats, giving shareholders negotiating leverage even when economically out of the money. This dynamic can influence whether restructurings pursue going concern or liquidation strategies, sometimes inefficiently.

The Operational Reality Check

Financial analysis must be grounded in operational reality. Engaging operational consultants to assess business viability independently of management projections provides critical perspective. Can the business actually achieve projected improvements? Do customers and suppliers support continuation? Is the workforce stable and capable?

A 2025 case study involved a specialty manufacturer where DCF analysis suggested going concern value of $180 million versus OLV of $125 million—seemingly supporting operational restructuring. However, operational due diligence revealed that the company's primary customer (representing 47% of revenue) was actively qualifying alternative suppliers and unlikely to support long-term continuation. This operational insight shifted the strategy toward rapid asset sale, ultimately achieving $138 million through a controlled auction process that preserved some going concern premium while avoiding the risk of customer loss during a prolonged restructuring.

06 Current Market Dynamics and Emerging Trends

The 2024-2025 restructuring environment has been shaped by several distinctive factors that influence the going concern versus liquidation calculus:

Interest Rate Impact

Elevated interest rates have dual effects. First, higher discount rates reduce going concern present values, narrowing the gap with liquidation values. Second, increased debt service burdens have pushed otherwise viable businesses into distress, creating situations where operational health supports going concern value despite temporary financial stress. This has led to increased use of liability management transactions and out-of-court restructurings that preserve going concern value while right-sizing capital structures.

Private Equity Involvement

Private equity sponsors facing portfolio company distress increasingly pursue dual-track processes—simultaneously marketing businesses as going concerns while developing liquidation alternatives. This optionality maximizes value but requires careful management to avoid operational disruption. In current markets, approximately 42% of middle-market restructurings involve PE-backed companies, up from 31% in 2019-2020.

Technology and Intangible Assets

The growing importance of intangible assets complicates liquidation analysis. Software, data assets, and intellectual property often have limited standalone value outside operational context, supporting going concern approaches. However, certain IP assets (patents, trademarks, customer lists) can command substantial values in targeted sales, creating break-up opportunities.

ESG and Stakeholder Considerations

Environmental liabilities increasingly influence liquidation values, as buyers discount heavily for remediation obligations. Social considerations—particularly employment impacts—sometimes drive stakeholders toward going concern solutions even when pure financial analysis suggests liquidation. Governance failures that precipitated distress may necessitate management changes as a condition for going concern support.

07 Practical Implementation: The Valuation Process

Executing distressed company valuations requires structured process discipline:

Phase 1: Situation Assessment (Weeks 1-2): Rapid triage to understand distress drivers, liquidity runway, and stakeholder dynamics. Preliminary analysis of whether going concern viability exists or liquidation is inevitable.

Phase 2: Detailed Analysis (Weeks 3-6): Comprehensive financial modeling, operational assessment, and asset appraisals. Development of both going concern and liquidation scenarios with supporting documentation.

Phase 3: Strategy Formulation (Weeks 7-8): Integration of valuation conclusions with legal, operational, and stakeholder considerations to develop recommended restructuring approach. Sensitivity analysis around key assumptions.

Phase 4: Execution and Monitoring (Ongoing): Implementation of chosen strategy with continuous monitoring of actual performance against projections. Flexibility to pivot between approaches as circumstances evolve.

This timeline assumes adequate preparation and information access. In crisis situations with compressed timeframes, the process necessarily accelerates, though often with reduced analytical precision.

Key Takeaway: The choice between going concern and liquidation valuation is not merely a technical exercise—it fundamentally shapes restructuring strategy and stakeholder outcomes. Rigorous analysis of operational viability, realistic financial projections, and detailed asset recovery assessments must be integrated with stakeholder dynamics and market conditions to determine the value-maximizing path forward.

08 Conclusion: Navigating Complexity in Distressed Valuation

The valuation of distressed companies demands technical sophistication, operational insight, and pragmatic judgment. As restructuring activity continues at elevated levels through 2025-2026, the ability to accurately assess when going concern value exceeds liquidation alternatives—or vice versa—remains a critical competency for advisors, creditors, and investors.

The framework outlined here provides structure for this analysis, but each situation presents unique complexities requiring tailored approaches. The gap between going concern and liquidation value reflects the premium for operational continuity and integrated asset deployment—a premium that exists only when genuine business viability can be established and stakeholder support secured.

In practice, many optimal outcomes involve hybrid approaches: break-up strategies that preserve going concern value for viable segments while liquidating impaired assets, or controlled sale processes that capture going concern premiums through strategic buyer interest while maintaining liquidation as a backstop.

The technical demands of these analyses—from detailed DCF modeling with appropriate distress adjustments to asset-by-asset liquidation assessments—require sophisticated analytical tools and deep market knowledge. Professional platforms like iValuate have become increasingly valuable in enabling restructuring advisors to perform these complex valuations efficiently, integrating multiple methodologies and scenario analyses to support sound strategic decisions in time-sensitive distressed situations.

As market conditions continue evolving, the fundamental principles remain constant: rigorous analysis, realistic assumptions, and integration of financial metrics with operational reality. Whether the conclusion points toward operational restructuring supported by going concern value or value-maximizing liquidation, the quality of the underlying valuation analysis ultimately determines whether stakeholders achieve optimal recoveries in challenging circumstances.