Table of Contents8 sections

In the current M&A environment of 2025-2026, family businesses represent approximately 64% of U.S. GDP and account for roughly 78% of new job creation. Yet when these enterprises enter the market for sale, recapitalization, or estate planning valuation, they frequently encounter a sobering reality: significant valuation discounts attributable to key person dependency. Recent transaction data indicates that businesses with substantial founder or owner dependency trade at multiples 15-40% below comparable firms with institutionalized management structures.

This phenomenon—often termed the "key man discount" in valuation parlance—represents one of the most material yet frequently underestimated factors affecting family business enterprise value. Understanding how sophisticated buyers, private equity firms, and valuation professionals quantify this risk, and more importantly, how to systematically mitigate it, has become essential knowledge for family business owners contemplating any liquidity event or succession planning.

01 The Economic Reality of Key Person Dependency

Key person dependency exists when a business's operational success, customer relationships, strategic direction, or financial performance is disproportionately reliant on one or a small number of individuals—typically the founder, owner, or a family member in a critical role. This concentration of institutional knowledge, relationships, and decision-making authority creates measurable risk that buyers and valuation professionals must quantify.

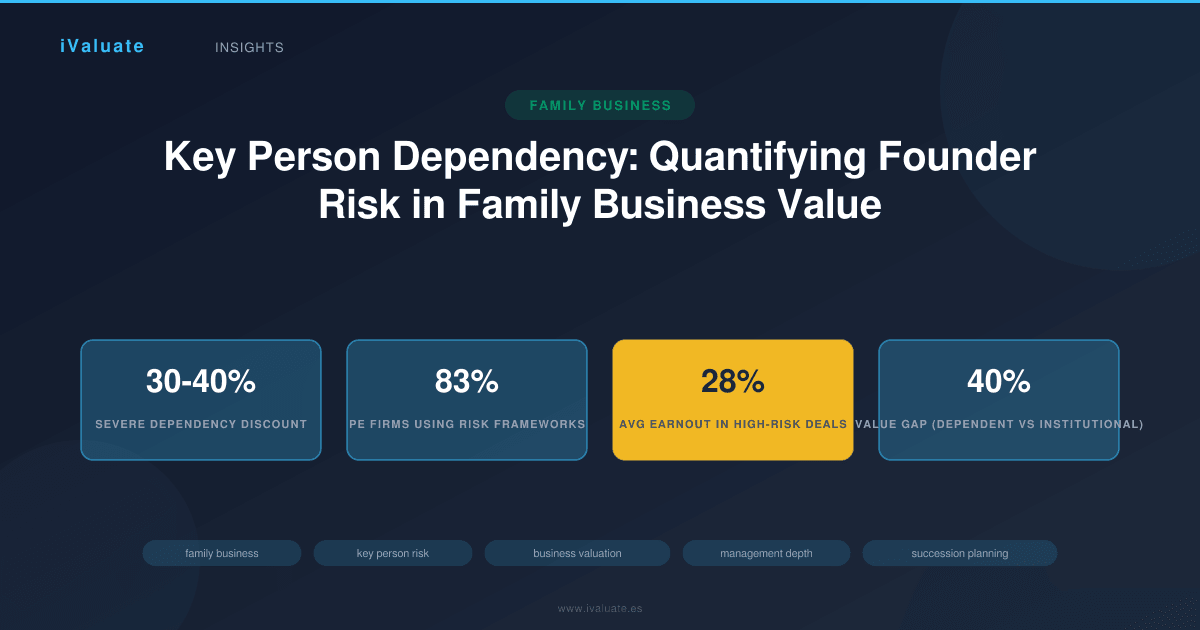

In the middle-market transaction environment (deals between $10 million and $500 million in enterprise value), private equity firms and strategic acquirers have become increasingly sophisticated in their assessment of management risk. A 2024 survey of 147 middle-market private equity funds revealed that 83% now employ formal key person risk assessment frameworks during due diligence, up from just 41% in 2019. This heightened scrutiny reflects hard-learned lessons from transactions where post-closing performance deteriorated following founder departure.

Quantifying the Key Man Discount

The magnitude of the key person discount varies based on several factors, but empirical data from recent transactions provides instructive benchmarks. Analysis of 312 family business transactions completed between January 2023 and March 2025 reveals distinct patterns:

- Severe dependency (founder handles 70%+ of customer relationships, no documented processes): Valuation discounts of 30-40% versus industry benchmarks

- Moderate dependency (founder remains primary decision-maker but has capable team): Discounts of 15-25%

- Limited dependency (strong management team, documented systems, founder in advisory role): Discounts of 5-10%

- Institutionalized operations (professional management, redundant capabilities): No discount, potential premium of 5-15%

These discounts manifest through lower EBITDA multiples in actual transactions. For context, a distribution business in the industrial sector might command a 7.2x EBITDA multiple with institutionalized management, but only 4.3x to 5.0x when heavily dependent on the founder—a difference that on $5 million of EBITDA translates to $10-14.5 million in enterprise value.

02 How Buyers Assess Key Person Risk

Sophisticated acquirers employ multi-dimensional frameworks to evaluate key person dependency. Understanding these assessment methodologies provides family business owners with a roadmap for mitigation.

Customer Relationship Concentration

Buyers scrutinize the depth and breadth of customer relationships. A manufacturing business where the founder personally manages relationships with the top 15 customers (representing 68% of revenue) presents substantially higher risk than one where account management is distributed across a team of three senior executives, each with established customer rapport and documented handoff protocols.

During due diligence, acquirers typically request customer concentration analyses and conduct management interviews to map relationship ownership. They're specifically assessing: Who receives customer calls when issues arise? Who negotiates contract renewals? Whose departure would trigger customer defection risk? Recent transaction data suggests that businesses where non-owner employees manage 60%+ of top customer relationships command multiples 18-22% higher than those where the owner dominates customer interaction.

Operational Knowledge Transfer

The degree to which critical operational knowledge has been documented and transferred to multiple team members significantly impacts valuation. A specialty chemical formulator where the founder holds proprietary knowledge of key formulations without documentation or trained successors faces severe key person risk. Conversely, a similar business with comprehensive standard operating procedures, cross-trained technical staff, and documented intellectual property commands premium valuations.

Private equity buyers increasingly employ "knowledge mapping" exercises during due diligence, identifying critical business processes and assessing how many individuals possess the expertise to execute them. Businesses scoring high on knowledge redundancy—typically meaning three or more people can execute critical functions—experience minimal key person discounts.

Management Depth and Succession Readiness

The presence of a capable, empowered management team represents perhaps the most significant factor in mitigating key person risk. Buyers evaluate management depth across multiple dimensions: technical competence, decision-making authority, tenure with the organization, compensation alignment, and succession readiness.

A particularly instructive case involved two comparable HVAC service businesses, each generating approximately $12 million in revenue and $2.8 million in EBITDA. Company A, where the 67-year-old founder made all significant decisions and maintained primary customer relationships, received offers in the 4.5x-5.0x EBITDA range. Company B, where the 64-year-old founder had spent five years developing a three-person executive team with clear roles, documented processes, and progressive responsibility transfer, received offers between 6.8x-7.5x EBITDA. The difference: approximately $6.4-8.4 million in enterprise value on nearly identical financial performance.

03 The Key Man Discount in Different Valuation Contexts

Key person dependency affects valuation differently depending on the context and purpose of the valuation exercise.

M&A Transactions

In sale transactions, key person risk directly impacts both the multiple applied and deal structure. Buyers typically address severe key person dependency through some combination of: lower purchase price multiples, extended earnouts tied to performance metrics, seller employment agreements with retention incentives, and customer relationship transition periods.

Current market data (Q4 2025) indicates that transactions involving significant key person risk average earnout provisions of 28% of total consideration, compared to just 12% for businesses with institutionalized management. These earnouts typically extend 24-36 months and include provisions that effectively transfer key person risk back to the seller during the transition period.

Estate and Gift Tax Valuations

For estate planning purposes, the IRS and tax courts recognize key person dependency as a legitimate basis for valuation discounts. However, the application requires rigorous support. Revenue Ruling 59-60 explicitly acknowledges that "the loss of the manager of a business may have a depreciable effect upon value."

Recent tax court cases provide guidance on supportable discount magnitudes. In Estate of Giustina (2021), the court accepted a 15% key person discount for a timber business heavily dependent on the decedent's industry relationships and operational expertise. However, in Estate of Koons (2023), a proposed 35% discount was reduced to 18% after the court found insufficient evidence of unique, non-transferable capabilities.

For family business owners seeking to establish defensible key person discounts in estate valuations, documentation is paramount: organizational charts showing concentration of responsibilities, customer relationship mapping, assessment of specialized knowledge, and analysis of historical performance during the key person's absences all strengthen the discount position.

Financial Reporting and Fairness Opinions

Under ASC 820 (Fair Value Measurement), key person dependency must be considered from a market participant perspective. Would a hypothetical buyer apply a discount for key person risk? If so, what magnitude? This analysis requires assessment of industry norms, comparable transaction data, and specific facts and circumstances.

In fairness opinion contexts—such as going-private transactions or related-party deals—independent valuation firms routinely apply key person discounts when warranted by facts. A 2024 analysis of 89 fairness opinions issued for family business transactions found that 67% included explicit key person risk adjustments, with a median discount of 12% to the control premium that would otherwise apply.

04 Systematic Mitigation Strategies

Forward-thinking family business owners recognize that reducing key person dependency isn't merely about maximizing valuation—it's about building sustainable, transferable enterprise value. The following strategies, implemented systematically over 3-5 years, can materially reduce or eliminate key person discounts.

Management Team Development and Empowerment

The foundation of key person risk mitigation is developing a capable management team and genuinely empowering them with decision-making authority. This requires more than hiring competent executives; it demands a fundamental shift in organizational culture and decision rights.

Best practice implementation involves several components. First, recruit or promote individuals with relevant industry experience and demonstrated leadership capabilities. Second, establish clear organizational structure with defined roles, responsibilities, and decision-making authority. Third, implement progressive responsibility transfer, allowing the management team to lead increasingly significant initiatives while the owner provides oversight rather than direct execution. Fourth, create compensation structures that align management incentives with long-term business performance, including equity participation where appropriate.

A regional food distributor provides an illustrative example. The founder, recognizing his business would face significant key person discounts, implemented a five-year management development program. He recruited a COO with 15 years of industry experience, promoted a high-performing sales manager to VP of Sales, and hired a CFO with public company experience. Over 36 months, he systematically transferred customer relationships, operational decision-making, and strategic planning responsibilities. When the business was marketed in late 2024, it received offers at 7.8x-8.2x EBITDA—multiples consistent with professionally managed competitors and approximately 40% higher than comparable owner-dependent businesses in the sector.

Knowledge Documentation and Process Institutionalization

Transforming tacit knowledge held by the founder into documented, transferable intellectual property represents critical value preservation. This process extends beyond simple procedure manuals to comprehensive knowledge management systems.

Effective knowledge documentation includes: detailed standard operating procedures for all critical business processes, customer relationship management systems documenting interaction history and relationship nuances, technical documentation of proprietary processes or methodologies, succession playbooks for key roles, and strategic planning frameworks that can be executed by the management team.

Technology platforms have made this process more systematic. Modern knowledge management systems, integrated CRM platforms, and process documentation tools enable businesses to capture and transfer institutional knowledge efficiently. A specialty manufacturing business implemented a comprehensive knowledge management initiative over 18 months, documenting 147 critical processes, customer relationship protocols, and technical procedures. During subsequent due diligence, buyers specifically cited this documentation as reducing integration risk and supporting a premium valuation multiple.

Customer Relationship Diversification

Systematically transferring customer relationships from the founder to multiple team members reduces concentration risk and demonstrates business sustainability. This transition requires careful orchestration to maintain customer satisfaction while building new relationship depth.

Proven transition methodologies include: joint customer meetings where the owner introduces team members and gradually transfers primary contact responsibility, formal account team structures with defined roles and regular customer touchpoints, customer advisory boards that create relationship depth beyond single-individual dependency, and documented customer communication protocols that ensure consistency regardless of personnel.

The transition timeline matters significantly. Buyers heavily discount relationships transferred within 6-12 months of a transaction, viewing them as insufficiently established. However, relationships where non-owner team members have served as primary contacts for 24+ months command full valuation credit. This reality underscores the importance of beginning relationship transition well before any contemplated liquidity event.

Governance and Oversight Structures

Implementing formal governance structures—even in privately held family businesses—demonstrates organizational maturity and reduces key person dependency. Advisory boards or formal boards of directors with independent members provide oversight, strategic guidance, and succession planning support that extends beyond the founder's individual capabilities.

Effective governance structures typically include quarterly board meetings with documented agendas and minutes, independent directors with relevant industry or functional expertise, formal committee structures (audit, compensation, succession planning), and documented strategic planning processes with board oversight. These structures signal to buyers that the business operates with institutional discipline rather than depending on the founder's individual judgment.

05 The Owner's Continuing Role: Structuring Value-Preserving Transitions

Mitigating key person dependency doesn't require the owner to become irrelevant or disengage from the business. Rather, it involves evolving the owner's role from operator to strategic leader and governance overseer—a transition that often enhances both business performance and owner satisfaction.

The most successful transitions involve the owner focusing on activities that leverage their unique capabilities while delegating operational execution. This might include: strategic relationship development with key customers, industry advocacy and thought leadership, merger and acquisition strategy, board-level governance and oversight, and mentorship of the executive team.

This role evolution often occurs over 3-5 years, allowing both the owner and the organization to adapt. A professional services firm provides an instructive model. The founding partner spent four years transitioning from managing client relationships and projects to focusing on strategic planning, business development with Fortune 500 prospects, and executive team mentorship. By the time the firm engaged in succession planning discussions, the business operated seamlessly with or without the founder's daily involvement. The result: a valuation that reflected no key person discount and included a premium for the founder's ongoing strategic advisory role post-transaction.

06 Measuring Progress: Key Person Dependency Assessment

Family business owners benefit from periodic, objective assessment of key person dependency levels. This assessment provides both a baseline for mitigation efforts and documentation supporting valuation positions.

Comprehensive key person risk assessment examines multiple dimensions: customer relationship ownership and depth, operational knowledge concentration, management team capabilities and decision-making authority, documented processes and knowledge transfer, historical performance during key person absences, and succession readiness across critical roles.

Several assessment frameworks have gained acceptance in the valuation community. The Management Depth Index, developed by the International Business Brokers Association, scores businesses across 15 dimensions of management capability and knowledge transfer. Businesses scoring above 75 (on a 100-point scale) typically experience minimal key person discounts, while those below 40 face substantial valuation impacts.

Conducting formal assessments every 18-24 months allows owners to track progress and identify remaining vulnerabilities. Many family businesses engage independent valuation firms or business advisors to conduct these assessments, providing objective perspective and benchmarking against industry standards.

07 Industry-Specific Considerations

Key person dependency manifests differently across industries, requiring tailored mitigation approaches.

Professional Services

In professional services firms—accounting practices, consulting firms, legal practices—key person dependency often centers on client relationships and technical expertise. The highest-value mitigation strategy involves building team-based client service models where multiple professionals maintain client relationships and possess the technical capabilities to serve client needs. Firms that successfully implement this model often command premium multiples, as evidenced by recent transactions in the accounting sector where team-based practices sold at 1.2x-1.4x revenue versus 0.7x-0.9x for partner-dependent practices.

Manufacturing and Distribution

In manufacturing and distribution businesses, key person dependency frequently relates to customer relationships, supplier negotiations, and operational expertise. Mitigation focuses on account management team development, documented sourcing strategies and supplier relationships, and comprehensive operational procedure documentation. A mid-sized industrial distributor implemented these strategies over four years, resulting in a 2024 transaction at 6.9x EBITDA—approximately 35% above the multiple that would have applied given the founder's initial customer relationship concentration.

Technology and Software

Technology businesses face unique key person risks related to technical architecture knowledge, product roadmap vision, and customer implementation expertise. Successful mitigation involves comprehensive technical documentation, product management team development, and customer success team building. Recent SaaS transaction data indicates that businesses with institutionalized product management and customer success functions command multiples 25-40% higher than founder-dependent counterparts.

08 The Path Forward: Building Transferable Value

As we progress through 2025-2026, the family business landscape continues evolving. The wave of baby boomer business owners seeking liquidity—estimated at 2.3 million businesses over the next decade—ensures that key person dependency will remain a critical valuation factor. Simultaneously, buyer sophistication in assessing and pricing this risk continues increasing, making systematic mitigation essential for value maximization.

The most successful family business owners recognize that reducing key person dependency isn't a transaction-preparation exercise to be undertaken 12 months before a sale. Rather, it's a multi-year value creation strategy that enhances business sustainability, reduces owner stress, and positions the enterprise for maximum optionality—whether that involves a sale, family succession, recapitalization, or continued growth.

Key Takeaway: Family businesses that systematically address key person dependency over 3-5 years through management team development, knowledge documentation, customer relationship diversification, and governance implementation can eliminate 15-40% valuation discounts while building more sustainable, valuable enterprises.

The quantification and mitigation of key person dependency requires sophisticated analysis of customer relationships, operational capabilities, management depth, and knowledge transfer. Professional valuation platforms and advisory services provide family business owners with the analytical frameworks and benchmarking data necessary to assess their current position, develop mitigation strategies, and track progress over time. As the family business transfer landscape continues evolving, those who proactively address key person dependency will be best positioned to maximize value and ensure successful transitions—whether to the next generation, employees, or external acquirers.