Índice9 secciones

The geopolitical landscape of 2026 presents valuation professionals with unprecedented complexity. The confluence of renewed U.S. tariff policies, escalating EU-US trade tensions, persistent Middle East conflicts affecting energy markets, and fragmenting global supply chains has fundamentally altered how we assess business value and structure cross-border transactions. For CFOs, M&A advisors, and private equity professionals, the question is no longer whether to incorporate geopolitical risk into valuation models—but precisely how much premium to assign and which methodologies provide the most defensible results.

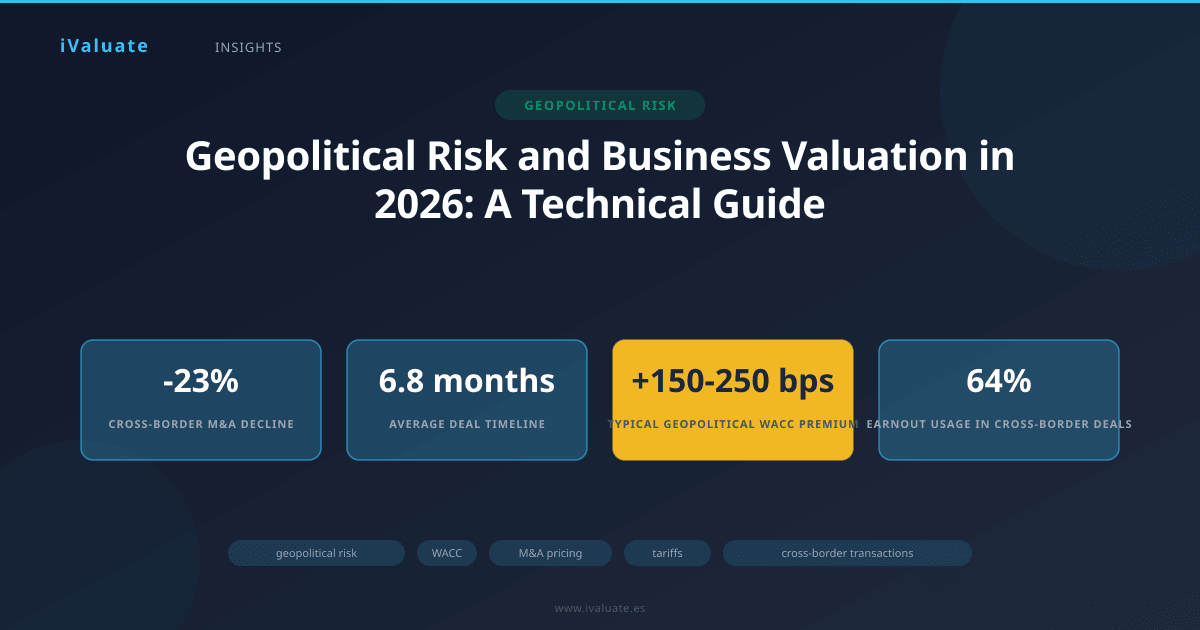

The data tells a stark story: cross-border M&A transaction volumes declined 23% in the first half of 2026 compared to the same period in 2024, while average deal completion times have extended from 4.2 months to 6.8 months. Meanwhile, the spread between domestic and international acquisition multiples has widened to levels not seen since the 2008 financial crisis. These aren't merely cyclical fluctuations—they represent structural shifts in how capital allocates across borders under conditions of sustained uncertainty.

01 The 2026 Tariff Regime: Quantifying Direct Valuation Impact

The Trump administration's return to aggressive trade policy in 2025 has created a tariff architecture significantly more complex than the 2018-2019 trade war. Current policy imposes baseline tariffs of 20% on most Chinese imports, 15% on European Union manufactured goods, and targeted sectoral tariffs reaching 35% on automotive components, steel, and advanced semiconductors. Retaliatory measures from trading partners have created effective tariff rates on U.S. exports averaging 18-22% across major markets.

From a valuation perspective, these tariffs create both immediate cash flow impacts and longer-term strategic uncertainties that must be reflected in discount rates. Consider a mid-market manufacturing company with $150 million in revenue, 40% of which derives from products containing imported components subject to the 20% baseline tariff. Assuming a 35% gross margin and inability to fully pass costs to customers, the tariff effectively reduces EBITDA by approximately $4.2 million annually—a 14% hit to enterprise value at typical manufacturing multiples of 7-8x EBITDA.

However, the direct cash flow impact represents only the first-order effect. Valuation professionals must also consider:

- Supply chain reconfiguration costs: Companies are spending 2-4% of revenue on supply chain diversification, with payback periods of 3-5 years

- Customer concentration risk: Tariffs disproportionately affect companies with >25% revenue from affected geographies

- Competitive dynamics: Domestically-focused competitors gain structural advantages, compressing multiples for internationally-exposed peers

- Policy uncertainty: The potential for tariff escalation or sudden policy reversals creates option value that traditional DCF models struggle to capture

In practice, we're observing valuation adjustments of 15-25% for companies with significant tariff exposure, implemented through a combination of reduced growth assumptions, increased WACC, and explicit scenario analysis with probability weighting.

02 WACC Recalibration: The Country Risk Premium Debate

The weighted average cost of capital remains the cornerstone of discounted cash flow valuation, and geopolitical risk manifests most directly through adjustments to the equity risk premium. The challenge for 2026 is that traditional country risk premium (CRP) methodologies—typically based on sovereign credit default swap spreads or bond yield differentials—fail to capture the granular, sector-specific nature of current geopolitical risks.

The conventional approach adds a country risk premium to the baseline equity risk premium when valuing businesses in emerging or politically unstable markets. Professor Aswath Damodaran's widely-used methodology calculates CRP as:

CRP = Default Spread × (σequity / σbond)

Where the default spread derives from sovereign bond yields and the ratio adjusts for equity volatility relative to bonds. For established markets like the United States or European Union, the CRP has historically approached zero. However, 2026 presents a fundamentally different environment.

We're now seeing sophisticated advisors apply modified CRPs even to developed market transactions based on:

- Sector-specific policy risk: Technology companies facing potential forced divestiture or data localization requirements may warrant 150-200 basis points of additional premium

- Supply chain geography: Companies with >30% of COGS sourced from geopolitically sensitive regions receive 100-175 basis point adjustments

- Revenue concentration: Businesses deriving >40% of revenue from markets subject to sanctions or trade restrictions see 125-225 basis point increases

- Regulatory complexity: Cross-border structures requiring multiple regulatory approvals in the current environment justify 75-150 basis point premiums

Consider a European industrial automation company being acquired by a U.S. private equity firm. The target generates 35% of revenue from China, sources 28% of components from Southeast Asia, and operates in a sector subject to export control scrutiny. A traditional WACC calculation might yield 9.5% (risk-free rate of 4.2%, equity risk premium of 6.0%, beta of 1.15). In the 2026 environment, defensible adjustments would include:

- Base WACC: 9.5%

- China revenue concentration premium: +1.5%

- Supply chain vulnerability premium: +1.0%

- Export control/regulatory premium: +0.8%

- Adjusted WACC: 12.8%

This 330 basis point adjustment translates to approximately 22% reduction in enterprise value for a business with stable cash flows and a 15-year projection period—a material impact that must be rigorously defended in fairness opinions and purchase price negotiations.

03 Middle East Conflict and Energy Sector Valuations

The ongoing instability in the Middle East has created particularly acute valuation challenges in the energy sector. Brent crude prices have oscillated between $72 and $118 per barrel in 2026, with volatility indices reaching levels 2.4x the 2020-2024 average. For energy companies, this volatility directly impacts reserve valuations, project economics, and the appropriate discount rates for long-lived assets.

The conflict's impact extends beyond commodity price volatility. Key valuation considerations include:

Shipping and logistics risk: Approximately 30% of global oil trade transits the Strait of Hormuz, with insurance premiums for tankers operating in the region increasing 400-600% since early 2025. Companies with significant Middle East exposure are seeing terminal value assumptions reduced by 12-18% to reflect the permanent risk premium associated with these supply routes.

Asset impairment triggers: Several major energy companies have taken $2-4 billion impairment charges on Middle Eastern assets in 2026, reflecting both immediate operational disruptions and longer-term questions about asset accessibility and development timelines. These impairments create precedents that affect comparable company analysis and transaction multiples across the sector.

Renewable energy arbitrage: Paradoxically, geopolitical instability in traditional energy regions has accelerated renewable energy valuations. European renewable developers are trading at EV/EBITDA multiples of 14-17x, compared to 11-13x for traditional energy infrastructure, reflecting a "geopolitical stability premium" that investors assign to assets insulated from Middle East risk.

A senior energy M&A advisor at a bulge bracket bank noted in a recent conference: "We're effectively running three valuation scenarios for every Middle East energy asset—stable operations, partial disruption, and complete loss of access. The probability weighting across these scenarios has become as important as the discount rate itself."

In a recent transaction involving a European energy major's acquisition of North Sea assets, the buyer successfully negotiated a 15% purchase price reduction by demonstrating that the seller's valuation model understated geopolitical risk. The buyer's analysis incorporated explicit modeling of supply disruption scenarios, insurance cost escalation, and the option value of geographic diversification—ultimately convincing the seller that the original 8.5% WACC was insufficient given the 2026 risk environment.

04 Cross-Border M&A: Deal Structures and Risk Allocation

Cross-border transaction volumes tell the story of 2026's geopolitical impact more clearly than any single metric. Total announced cross-border M&A reached $847 billion in the first three quarters of 2026, down from $1.1 trillion in the comparable 2024 period—a 23% decline that masks even more dramatic shifts in deal structure and risk allocation.

Traditional cross-border deals assumed relatively frictionless movement of capital, goods, and intellectual property across borders. The 2026 reality requires fundamentally different transaction architectures:

Earnout Structures and Geopolitical Contingencies

Earnouts have evolved from performance-based mechanisms to geopolitical risk-sharing tools. We're observing earnout provisions in 64% of cross-border deals over $100 million, compared to 38% in 2023-2024. These structures increasingly include:

- Tariff adjustment mechanisms: Purchase price adjustments triggered if tariff rates exceed specified thresholds, typically with 12-18 month lookback periods

- Regulatory approval contingencies: Extended earnout periods (36-48 months vs. traditional 24 months) that defer payment until regulatory uncertainty resolves

- Supply chain performance metrics: Earnout payments tied not just to revenue/EBITDA but to successful supply chain diversification milestones

- Currency and sanctions clauses: Explicit provisions addressing payment mechanisms if sanctions restrict normal banking channels

A representative transaction involved a U.S. technology company's acquisition of a German semiconductor equipment manufacturer. The deal structure included €180 million upfront (65% of total consideration) and €95 million in earnouts tied to: (1) achievement of 2027-2028 EBITDA targets (€45 million), (2) successful establishment of U.S. manufacturing capability (€30 million), and (3) maintenance of Chinese market access above 15% of revenue (€20 million). This structure effectively transferred geopolitical execution risk to the seller while providing upside participation if risks failed to materialize.

Escrow and Indemnification

Escrow provisions have expanded dramatically, with average escrow amounts reaching 18-22% of purchase price for cross-border deals, compared to 10-12% for domestic transactions. The duration of these escrows has extended to 24-36 months, reflecting the time required for geopolitical risks to manifest.

Indemnification provisions now routinely include carve-outs for "geopolitical events," creating complex negotiations around what constitutes a foreseeable vs. unforeseeable risk. A European private equity firm recently walked away from a $340 million cross-border acquisition when the seller refused to provide indemnification for losses resulting from tariff increases above 25%—the buyer's position being that such increases were reasonably foreseeable given current policy trajectories.

05 Sector-Specific Valuation Impacts

Technology and Semiconductors

The technology sector faces uniquely complex geopolitical valuation challenges in 2026. U.S.-China technology decoupling has accelerated, with the CHIPS Act restrictions, export controls on advanced semiconductors, and reciprocal Chinese limitations creating bifurcated markets. Companies serving both markets face the prospect of forced restructuring or market exit.

Semiconductor companies with significant China exposure (>25% of revenue) are trading at 15-20% discounts to purely Western-focused peers, even after controlling for growth rates and profitability. In M&A transactions, buyers are applying 200-300 basis point WACC premiums to cash flows derived from Chinese operations, and frequently modeling complete loss of China revenue in downside scenarios.

A notable 2026 transaction involved the acquisition of a fabless chip designer with 40% revenue from Chinese customers. The buyer's valuation model assigned only 30% probability to maintenance of Chinese market access beyond 2028, effectively writing down the present value of those cash flows by 70%. This approach reduced enterprise value by approximately $280 million (18% of the original seller's valuation) and became the primary point of negotiation.

Automotive and Manufacturing

Automotive sector valuations reflect the compound impact of tariffs, supply chain complexity, and the electric vehicle transition. Traditional automotive suppliers with global footprints are experiencing multiple compression, with median EV/EBITDA multiples declining from 6.8x in 2024 to 5.2x in 2026 for companies with >35% international revenue exposure.

The valuation challenge stems from the sector's extended supply chains—a typical vehicle contains components from 8-12 countries, each potentially subject to different tariff regimes. Companies are responding by regionalizing supply chains, but this restructuring requires capital investment of 3-5% of revenue annually for 3-4 years, with uncertain returns.

Private equity interest in the sector has shifted dramatically toward pure-play domestic suppliers or companies with fully regionalized supply chains. A recent auction for a Tier 2 automotive supplier attracted 12 initial bidders but only 3 final round participants—all domestic strategic buyers. The winning bid of 5.4x EBITDA represented a 22% discount to the seller's initial expectations, with the valuation gap attributed entirely to geopolitical risk factors.

Consumer and Retail

Consumer companies with Asian manufacturing bases face direct tariff impacts on landed costs, but also longer-term strategic questions about brand positioning and consumer sentiment. We're observing a "reshoring premium" in valuations, with companies that have successfully moved 50%+ of manufacturing to Western hemisphere locations commanding 12-15% higher multiples than comparable peers still dependent on Asian production.

The calculus involves not just current tariff costs but the option value of geographic flexibility. A consumer electronics company that completed a $45 million investment in Mexican manufacturing capacity saw its acquisition multiple increase from 9.2x to 10.8x EBITDA within 18 months—the market rewarding the strategic flexibility even though Mexican production costs were 8-12% higher than the previous Chinese manufacturing base.

06 Practical Implementation: Adjusting Your Valuation Models

For valuation professionals navigating the 2026 environment, several practical frameworks have emerged as best practices:

Scenario-Based DCF Analysis

Traditional single-point DCF models are insufficient for capturing geopolitical risk. Leading practitioners now employ probability-weighted scenario analysis with at least three distinct scenarios:

- Base case (50-60% probability): Current geopolitical tensions persist but don't materially escalate; tariffs remain at current levels; supply chains adapt over 2-3 years

- Adverse case (25-35% probability): Significant escalation in trade tensions; tariff rates increase 30-50%; potential sanctions or market access restrictions; supply chain disruptions

- Favorable case (10-20% probability): De-escalation of tensions; tariff reductions; improved trade relationships; normalization of cross-border commerce

Each scenario requires distinct assumptions for revenue growth, margin profiles, capital requirements, and discount rates. The probability-weighted result provides a more defensible valuation than attempting to capture all risks in a single discount rate adjustment.

Explicit Risk Premium Documentation

Given the heightened scrutiny of cross-border valuations by boards, regulators, and courts, documentation of risk premium assumptions has become critical. Best practice includes:

- Quantitative analysis linking specific geopolitical exposures to basis point adjustments

- Peer company analysis showing how public market valuations reflect similar risks

- Sensitivity analysis demonstrating valuation impact of different risk premium assumptions

- Third-party data sources (country risk ratings, political risk insurance pricing, CDS spreads) supporting the chosen premiums

Dynamic Monitoring and Revaluation Triggers

The rapid pace of geopolitical change in 2026 requires more frequent valuation updates than traditional annual or quarterly cycles. Leading organizations have implemented trigger-based revaluation protocols that mandate updated analyses when:

- Tariff rates change by more than 5 percentage points

- New sanctions are imposed affecting >10% of revenue or supply chain

- Major geopolitical events occur (conflicts, regime changes, trade agreement terminations)

- Regulatory approval timelines extend beyond 6 months past initial expectations

For portfolio companies and acquisition targets, this dynamic approach ensures that valuations reflect current reality rather than outdated assumptions—critical for accurate financial reporting, fundraising, and transaction execution.

07 The Role of Political Risk Insurance in Valuation

Political risk insurance (PRI) has evolved from a niche product to a mainstream tool for managing and quantifying geopolitical risk in M&A transactions. The PRI market has grown approximately 35% annually since 2024, with premium volumes exceeding $4.2 billion in 2026.

From a valuation perspective, PRI serves two critical functions. First, it provides objective, market-based pricing of specific geopolitical risks—effectively offering a third-party validation of risk premium assumptions. When an insurer quotes 180 basis points annually to cover expropriation and political violence risks for a specific asset, that premium provides a floor for the risk adjustment that should appear in WACC calculations.

Second, PRI can fundamentally alter deal economics by transferring tail risks from buyer to insurer. In a recent $520 million cross-border acquisition, the buyer secured comprehensive PRI coverage for $8.7 million annually (167 basis points on transaction value). This insurance enabled the buyer to reduce the geopolitical risk premium in its WACC from 250 basis points to 100 basis points, increasing the supportable purchase price by approximately $65 million—more than covering seven years of insurance premiums.

However, PRI has limitations. Policies typically exclude "normal" trade policy changes, covering only dramatic events like expropriation, political violence, or currency inconvertibility. The gradual erosion of value from escalating tariffs or regulatory restrictions—precisely the risks most relevant in 2026—often falls outside standard coverage.

08 Looking Forward: Structural Changes in Global Capital Allocation

The geopolitical environment of 2026 represents more than a cyclical downturn in cross-border activity—it reflects a structural shift in how global capital markets function. The post-Cold War era of increasing economic integration and declining barriers to cross-border commerce has given way to a more fragmented, regionalized system.

For valuation professionals, this shift has several implications that will persist beyond current policy cycles:

Permanent risk premiums: Even if specific tariffs are reduced or trade tensions ease, the demonstrated willingness of governments to use economic policy as geopolitical leverage has created a permanent option value that markets will continue to price. Country risk premiums for developed markets, once assumed to be zero, will likely stabilize at 75-150 basis points for the foreseeable future.

Regionalization premium: Companies with regional rather than global footprints will command structural valuation premiums. The complexity discount that once applied to geographically concentrated businesses has inverted—simplicity and regional focus now carry premium valuations.

Optionality and flexibility: Traditional DCF models assume relatively static business configurations. The 2026 environment rewards flexibility—the ability to shift supply chains, redirect sales efforts, or restructure operations in response to policy changes. Valuation methodologies must evolve to capture this option value, potentially incorporating real options analysis for major strategic decisions.

ESG integration: Geopolitical risk increasingly intersects with environmental, social, and governance considerations. Supply chain decisions driven by tariff avoidance have ESG implications; energy security concerns affect climate transition timelines; human rights considerations influence market access. Valuation models must integrate these interconnected risks rather than treating them as separate analytical silos.

The private equity industry has adapted most quickly to this new reality, with leading firms establishing dedicated geopolitical risk teams and integrating political risk analysis into investment committee processes. Public company CFOs and corporate development teams are following suit, recognizing that geopolitical risk management has become a core competency rather than a peripheral concern.

09 Conclusion: Rigor and Adaptability in Uncertain Times

The geopolitical landscape of 2026 demands that valuation professionals elevate their analytical rigor while embracing greater uncertainty in their models. The comfortable assumptions of the 2010-2020 period—stable trade relationships, predictable regulatory environments, and minimal country risk in developed markets—no longer hold. The spread between domestic and cross-border acquisition multiples, the proliferation of earnout structures, and the dramatic expansion of WACC adjustments all reflect a market grappling with fundamentally higher levels of uncertainty.

Yet this environment also creates opportunities for differentiation. Advisors who develop sophisticated frameworks for quantifying geopolitical risk, who can defend their assumptions with rigorous analysis and market data, and who structure transactions to appropriately allocate these risks between parties will deliver superior outcomes for their clients. The gap between sophisticated and simplistic geopolitical risk analysis can easily represent 15-25% of enterprise value in affected transactions—making this expertise among the most valuable skills in the current M&A environment.

For organizations seeking to navigate these complexities, the integration of geopolitical risk analysis into standard valuation workflows is no longer optional. Whether you're a CFO preparing for a board valuation discussion, a private equity professional underwriting a new investment, or an M&A advisor opining on fairness, your analysis must explicitly address how trade policies, sanctions regimes, and political instability affect value. The tools and methodologies for this analysis continue to evolve, and platforms like iValuate are increasingly incorporating geopolitical risk modules that help professionals perform these complex analyses efficiently and defensibly.

The geopolitical uncertainty of 2026 will eventually resolve—specific trade disputes will settle, particular conflicts will end, and policy regimes will change. But the fundamental lesson of this period will endure: geopolitical risk is not an exotic consideration for frontier markets but a core component of valuation analysis for businesses operating anywhere in an interconnected global economy. The professionals who master this reality will be best positioned to serve their clients through whatever geopolitical environment emerges in the years ahead.